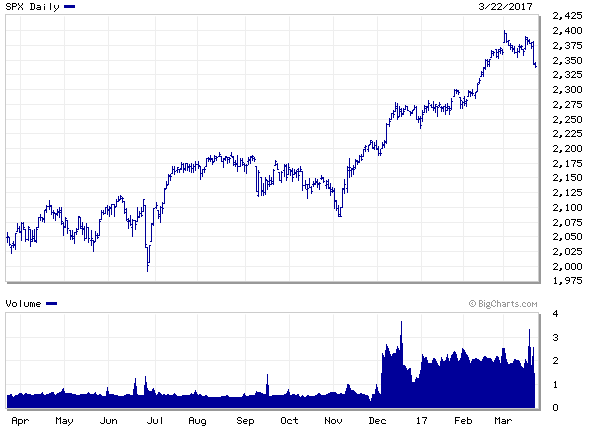

The year is off to a great start for stock investors, as the S&P 500 Index (U.S. large companies) is up 6.07% through the end of March. U.S. stocks have been strong over the course of the last several years, as we’ve seen only minor declines often followed by broad-based rallies. The most recent rally goes all the way back to the day after the U.S. Presidential Election, when the market decided that a Trump presidency may actually be good for stocks, due to the possibility of massive corporate tax reform. The proposed changes to the tax code could greatly increase corporate profit margins. Since the election, markets have experienced only one trading day in which the S&P 500 fell farther than 1%, the longest streak since the bull market of the 1990s.

It was not only U.S. stocks that performed well over the course of the first quarter. The MSCI World ex USA Index (International companies) has risen over 6.81% so far this year, which is unusual in light of the severe underperformance of international stocks over the last several years. Another shift in the first quarter was that small companies underperformed after a year of very large gains. The Russell 2000 Index returned just 2.47%.

On the fixed income side, despite the Federal Reserve raising the Federal Funds rate to 1% from 0.75% at the March meeting, bond yields and prices were relatively unchanged from the beginning of the year. (Bond yields rise as prices fall). It appears that the market anticipated the rate hike and adjusted accordingly. It’s expected that the Federal Reserve will raise rates at least two more times this year, in 0.25% increments. While yields were stagnant this quarter, they have risen a dramatic 34% over the course of the last year, as evidenced by the U.S. 10 year yield chart below.

If you have questions about your investments, feel free to give us a call.